Technology

Nitrogen Producer Competitiveness Squeezed $70/Tonne in new Era Energy Pricing

Impact of energy on the nitrogen market

(Source: Integer Research )

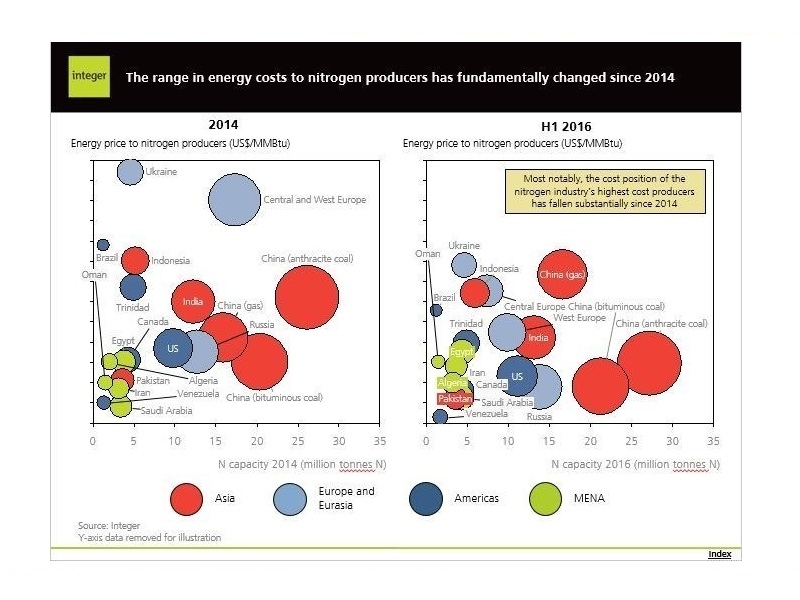

(Source: Integer Research )

Integer Research has conducted research into the impact of energy on the nitrogen market and the outlook for feedstock costs which shows that the range between the highest and lowest cost producers in the market has been squeezed across all nitrogen products by as much as $70 per tonne in the last year alone. This new era of energy pricing and its impact across the nitrogen market is analysed in Integer's new energy focus report.

The analysis of energy market dynamics is essential to understand the economics of the global nitrogen industry. Nitrogen prices are fundamentally linked to the price of energy since most nitrogen producers worldwide utilise natural gas or coal as their feedstock, and the main cost component of nitrogen production is energy.

Market prices for gas and coal increasingly reflect a complex combination of national, regional and/or global supply and demand for gas. Integer's view is that the development of these factors is what will determine the future competitive position of nitrogen producers on the global cost curve - and this is reflected in Integer's medium and long term global producer cost curves.

Market prices for gas and coal increasingly reflect a complex combination of national, regional and/or global supply and demand for gas. Integer's view is that the development of these factors is what will determine the future competitive position of nitrogen producers on the global cost curve - and this is reflected in Integer's medium and long term global producer cost curves.

For nitrogen producers with market-priced feedstock costs, profitability and competitive position is largely a function of underlying energy market factors.

The global energy market has fundamentally changed in recent years, and further change is on the horizon. Perceived energy scarcity has given way to a new era of energy abundance due to the growth of newly advanced developing economies, particularly China, and technological innovation in the oil and natural gas industry, giving rise to shale gas and increased LNG trade.

The global energy market has fundamentally changed in recent years, and further change is on the horizon. Perceived energy scarcity has given way to a new era of energy abundance due to the growth of newly advanced developing economies, particularly China, and technological innovation in the oil and natural gas industry, giving rise to shale gas and increased LNG trade.

Integer comprehensively scrutinise the nature of gas and coal pricing to nitrogen producers, in the new focus report on the impact of energy on the nitrogen market and the outlook for feedstock costs and product prices.

Selected key findings :

* Saudi Arabia's fixed-gas price increased by US$0.75/MMBtu to US$1.50/MMBtu from 1 January 2016, causing the country to move up the global urea cost curve. Meanwhile, producers in Europe reaped the benefits of continued low hub-based gas prices, and bituminous and anthracite coal prices in China continued to fall albeit at slower rates.

Selected key findings :

* Saudi Arabia's fixed-gas price increased by US$0.75/MMBtu to US$1.50/MMBtu from 1 January 2016, causing the country to move up the global urea cost curve. Meanwhile, producers in Europe reaped the benefits of continued low hub-based gas prices, and bituminous and anthracite coal prices in China continued to fall albeit at slower rates.

* Although Ukraine's gas costs fell to US$7.8/MMBtu on average in H1 2016 as it diversified away from Russian gas towards cheaper European imports, the country moved towards the top of the global cost curve given the relative decrease in gas costs in other regions.

* In China, natural-gas based urea production moved further up the cost curve due to government restrictions on gas supply which resulted in higher fixed gas prices to nitrogen plants.

* In China, natural-gas based urea production moved further up the cost curve due to government restrictions on gas supply which resulted in higher fixed gas prices to nitrogen plants.

* The global range in ammonia ex-works production costs contracted by US$70 per tonne to US$241 per tonne in the first half of 2016 compared to 2015, as feedstock prices continued to decline globally, particularly in countries where gas prices are market-driven such as the US and Europe. This led to producers with regulated or fixed gas prices, such as in Saudi Arabia and Egypt, becoming comparatively less competitive.

* European producers have shown the largest fall in ex-works urea production costs compared to 2015, due to sustained low hub-based gas prices, while Saudi Arabia, Iran and Nigeria are among the countries that have experienced year-on-year increases in gas costs due to revised state regulated gas prices.

* European producers have shown the largest fall in ex-works urea production costs compared to 2015, due to sustained low hub-based gas prices, while Saudi Arabia, Iran and Nigeria are among the countries that have experienced year-on-year increases in gas costs due to revised state regulated gas prices.

* Compared to the annual average gas price in 2015, Russia moved up the global nitrates cost curve in rouble terms however remained cost competitive in US dollar terms due to continued devaluation of the rouble. Producers in West Europe moved further down the cost curve as a result of falling market based gas prices, and improved their profitability even more so due to the sustained price premium in effect in Europe.

Source : Integer Research

Ruby BIRD

http://www.portfolio.uspa24.com/

Yasmina BEDDOU

http://www.yasmina-beddou.uspa24.com/

Source : Integer Research

Ruby BIRD

http://www.portfolio.uspa24.com/

Yasmina BEDDOU

http://www.yasmina-beddou.uspa24.com/

Liability for this article lies with the author, who also holds the copyright. Editorial content from USPA may be quoted on other websites as long as the quote comprises no more than 5% of the entire text, is marked as such and the source is named (via hyperlink).